This little chart I stole from a recent edition of “The Economist” I’ll paste the article below

Or listen here:

https://podcastaddict.com/podcast/economist-podcasts/4046013 via @PodcastAddict

THE SUN MACHINES

NAIVE EXTRAPOLATION HAS TROUNCED SOBER FORECASTING AGAIN AND AGAIN

The Economist (North America)

APHOTOVOLTAIC CELL is a very simple thing: a square piece of silicon typically 182 millimetres on each side and about a fifth of a millimetre thick, with thin wires on the front and an electrical contact on the back. Shine light on it, and an electric potential—a voltage—will build up across the silicon: hence “photovoltaic”, or PV.

Run a circuit between the front and the back, and in direct sunlight that potential can provide about seven watts of electric power.

This year the world will make something like 70bn of these solar cells, the vast majority of them in China, and sandwich them between sheets of glass to make what the industry calls modules but most other people call panels: 60 to 72 cells at a time, typically, for most of the modules which end up on residential roofs, more for those destined for commercial plant. Those panels will provide power to family homes, to local electricity collectives, to specific industrial installations and to large electric grids; they will sit unnoticed on roofs, charmingly outside rural schools, controversially across pristine deserts, prosaically on the balconies of blocks of flats and in almost every other setting imaginable.

Once in place they will sit there for decades, making no noise, emitting no fumes, using no resources, costing almost nothing and generating power. It is the least obtrusive revolution imaginable. But it is a revolution nonetheless.

Over the course of 2023 the world’s solar cells, their panels currently covering less than 10,000 square kilometres, produced about 1,600 terawatt-hours of energy (a terawatt, or 1TW, is a trillion watts). That represented about 6% of the electricity generated world wide, and just over 1% of the world’s primary-energy use. That last figure sounds fairly marginal, though rather less so when you consider that the fossil fuels which provide most of the world’s primary energy are much less efficient. More than half the primary energy in coal and oil ends up as waste heat, rather than electricity or forward motion.

What makes solar energy revolutionary is the rate

of growth which brought it to this just-beyond-the-marginal state. Michael Liebreich, a veteran analyst of clean-energy technology and economics, puts it this way: in 2004, it took the world a whole year to install a gigawatt of solar-power capacity (1GW is a billion watts, or a thousandth of a terawatt); in 2010, it took a month; in 2016, a week. In 2023 there were single days which saw a gigawatt of installation worldwide. Over the course of 2024 analysts at BloombergNEF, a data outfit, expect to see 520-655GW of capacity installed: that’s up to two 2004s a day.

This extraordinary growth stems from the interplay of three simple factors. When industries make more of something, they make it more cheaply. When things get cheaper, demand for them grows. When demand grows, more is made. In the case of solar power, demand was created and sustained by subsidies early this century for long enough that falling prices became noteworthy and, soon afterwards, predictable. The positive feedback that drives exponential growth took off on a global scale.

And it shows no signs of stopping, or even slowing down. Buying and installing solar panels is currently the largest single category of investment in electricity generation, according to the International Energy Agency ( IEA), an intergovernmental think-tank: it expects $500bn this year, not far short of the sum being put into upstream oil and gas. Installed capacity is doubling every three years. According to the International Solar Energy Society, solar power is on track to generate more electricity than all the world’s nuclear power plants in 2026, than its wind turbines in 2027, than its dams in 2028, its gas-fired power plants in 2030 and its coal-fired ones in 2032. In an IEA scenario which provides net-zero carbon-dioxide emissions by the middle of the century, solar energy becomes humankind’s largest source of primary energy—not just electricity—by the 2040s.

Growth in solar is not dependent on efforts to stabilise the climate; if it keeps getting cheaper it will grow even if people persist in burning coal and oil alongside it. In a paper published in 2022 Rupert Way of Oxford University and colleagues sought to see what would happen if the costs of solar and other new technologies kept falling with increased deployment as they have done in the past. Under their “fast transition” scenario, they found that by 2070 the world could be getting more useful energy from solar cells than it got from all energy sources combined last year (see chart on subsequent page).

Expecting exponentials to carry on is rarely a basis for sober forecasting. At some point either demand or supply faces an unavoidable constraint; a graph which was going up exponentially starts to take on the form of an elongated S. And there is a wide variety of plausible stories about possible constraints, from manufacturers going bust, to solar farms not being able to connect to grids, to extensively solar-powered grids not being stable, to excessively solar grids no longer being attractive sites for further investment.

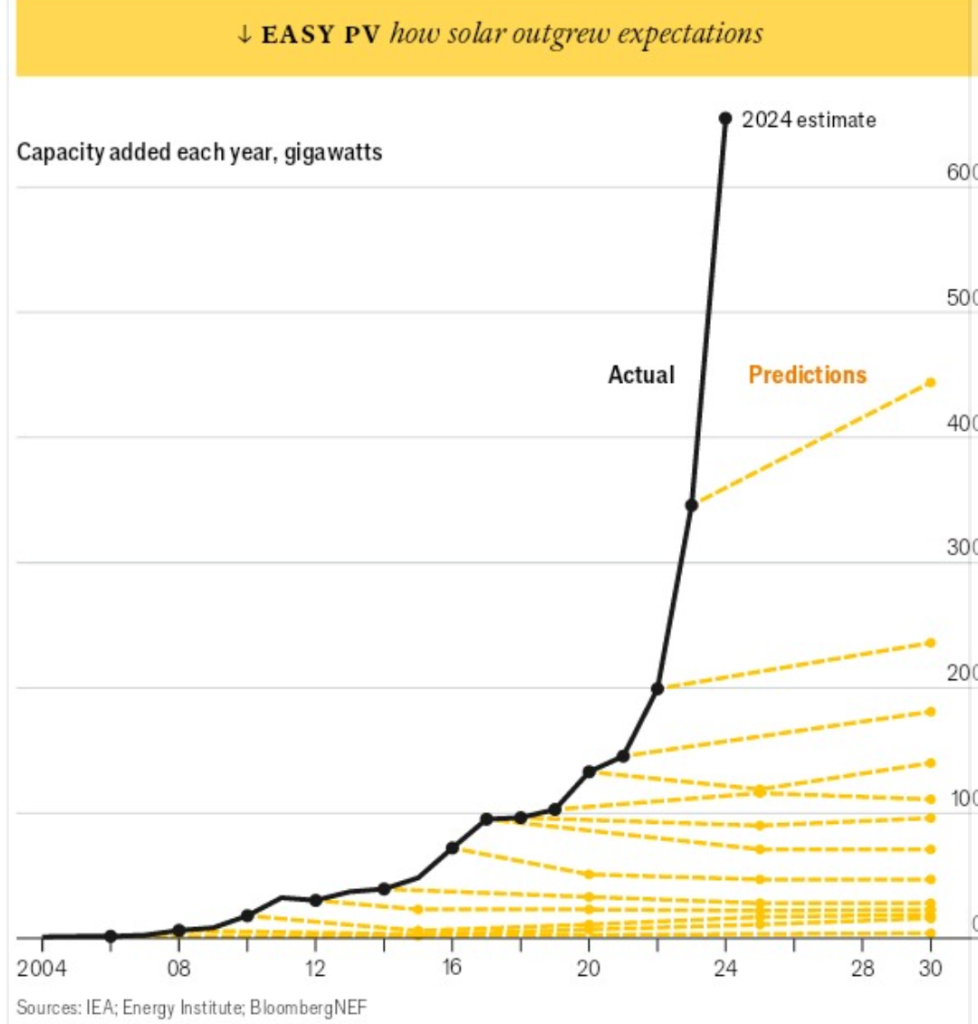

All real issues. But the past 20 years of solar growth have seen naive extrapolations trounce forecasting soberly informed by such concerns again and again. In 2009, when installed solar capacity worldwide was 23GW, the energy experts at the IEA predicted that in the 20 years to 2030 it would increase to 244GW. It hit that milestone in 2016, when only six of the 20 years had passed. According to Nat Bullard, an energy analyst, over most of the 2010s actual solar installations typically beat the IEA’s five-year forecasts by 235% (see chart). The people who have come closest to predicting what has actually happened have been environmentalists poo-pooed for zealotry and economic illiteracy, such as those at Greenpeace who, also in 2009, predicted 921GW of solar capacity by 2030. Yet even that was an underestimate. The world’s solar capacity hit 1,419GW last year.

This performance suggests that solar is not like other energy sources. History shows the same thing. From 1800 to 2020 the amount of energy the world derived from coal increased by roughly a factor of 400. But as Dr Way and his colleagues point out, when adjusted for inflation coal’s cost in terms of its energy content stayed more or less the same. The same is true for the long-term costs of oil and, later, natural gas. Exploiting these fuels drove lots of economic growth; that made the fuels more affordable, their use more valuable and the returns on their production greater. But their costs stayed broadly stable in real terms.

Since the 1960s what analysts call the levelised cost of solar energy—the break-even price a project needs to get paid in order to recoup its financing for a fixed rate of return—has dropped by a factor of more than 1,000, and the trend is continuing. Now that solar energy is a significant part of the world’s entire energy portfolio, the world as a whole is going to go on seeing the energy used in many applications getting cheaper and cheaper. A burst of innovation aimed at making the most of this bonanza will change the way many existing industries work and create new ones more or less from scratch. It will be the steepest drop in the price of one of the basic factors of production that the world economy has ever seen.

THE CYLINDERS for the first steam engines that Matthew Boulton and James Watt began to sell in the 1770s were not made in-house at Boulton’s Soho manufactory, outside Birmingham; they were cast at the nearby foundry of John “Iron Mad” Wilkinson. But the manufactory provided the fittings that turned those cylinders into engines, supervised the engines’ building and owned the patent on their design. As Boulton explained to James Boswell, a writer, when he visited the Soho works, “I sell here, Sir, what all the world desires to have—power.”

The silicon foundries of China lack salesmen with Boulton’s verve (“an iron chieftain…father to his tribe,” as Boswell put it). But when it comes to exquisite chemical purity and physical flawlessness, the wares they provide to serve the world’s desire for power should be enough to make anyone silicon mad.

Their raw material is sand made of quartz, a crystalline form of oxidised silicon. Silicon foundries heat it to 1,900°C in electric-arc furnaces with some carbon, in the form of coke. The oxygen from the sand reacts with the carbon to create carbon monoxide, leaving behind molten “polysilicon”. That is then cooled, crushed and reacted with hydrochloric acid to produce a volatile liquid called trichlorosilane, which is then repeatedly distilled to remove all trace of impurity. The most advanced foundries work at “10 nines”, meaning that polysilicon they derive from their trichlorosilane is 99.99999999% pure. This silicon can then be remelted and cooled in a way which sees every atom end up sitting in its properly appointed spot within a single crystal.

Until the beginning of this century the only products that were worth this sort of palaver were the wafers from which the computer industry made its silicon chips. The solar-cell industry lived on the offcuts. But the subsidies of the mid-2000s saw demand for photovoltaics rise beyond what the computer industry could spare. As the price of polysilicon rose, firms in Asia started to make the investments needed to build polysilicon foundries for supplying the PV industry.

China quickly took the lead, and kept it. In 2023 Chinese firms made 93% of all the world’s polysilicon destined for solar cells. Some are vertically integrated and make photovoltaics themselves (an approach Boulton took when he invested in a foundry of his own at Soho). Some leave the diamond-saw slicing of their ingots into wafers, the precise polishing of their surfaces and the perfectly calibrated “doping” that makes the silicon into a semiconductor to their customers.

The country’s foundries and manufacturers have followed extraordinarily bullish investment strategies. But as Mr Bullard explains, if as a manufacturer you are tempted to heed a forecast of solar installation that rises only gently, “you are dead the second you look at that line.” It is all-in all the time.

That said, the manufacturers benefit from the fact that they are key to their country’s industrial strategy. There have been some bankruptcies, but the Chinese government has extended cheap loans to many overextended firms. Gregory Nemet of the University of Wisconsin-Madison notes that the solar-cell market typically catches up with the overcapacity thus created within a couple of years. The current oversupply will see whether this remains the case. China’s two biggest producers of polysilicon, GCL- Poly and Tongwei, each had a production capacity of 370,000 tonnes in 2023, more than enough to meet demand. Tongwei has said it is investing some $3.9bn in a new facility that will eventually be able to produce 400,000 tonnes a year. Johannes Bernreuter, an analyst of the polysilicon market, says China has facilities capable of 7m tonnes a year in the pipeline, enough to produce an annual 3.5TW of solar panels.

In terms of polysilicon such amounts are seen as huge. But it is worth noting that in terms of the material requirements of other energy technologies they are tiny. Coal production runs at roughly 8bn tonnes a year; add on oil and gas and you double that.

Chinese firms have other advantages, notably a vast and protected domestic market and low-cost energy. GCL- Poly and other Chinese firms have several factories in Xinjiang near huge coal-fired power plants which themselves sit more or less on top of large coal mines. Electricity accounts for 40% of the cost of polysilicon production, and burning coal that was mined next door in a depreciated plant that delivers power to your arc furnaces directly is pretty cheap. That said, before too long solar power could be cheaper.

Though protected and subsidised—and open, in Xinjiang, to allegations of the use of forced labour— the Chinese industry is also fiercely competitive in the sort of way that only companies manufacturing more or less the same thing can be. Manufacturers of other energy technologies have to keep the specific needs of their various clients in mind. Engines which burn fuel are dramatically different depending on whether they are to be installed in a back-up generator or a moped. Turbines which spin under the force of moving fluids must be tailored to the steam of a coal plant or the water of a hydroelectric plant. Such specialisation produces the sort of friction and lock-in that favours incumbents. Siemens has been able to hold its edge in the manufacture of gas turbines for decades.

In PVs, though, there is no such enduring edge to be found. Solar cells are standardised products all made in basically the same way; they have no moving parts at all, let alone the fiendish complexity of a modern turbine. Manufacturers compete on cost, by either making cells that make fractionally more electricity out of a given amount of sunshine or which cost less. “The barriers to entry are capex,” says Jenny Chase, who analyses the industry at BloombergNEF. “You can buy the machines [needed for manufacture], it’s not super tech-intensive.”

The commoditised nature of the product does not just lead to relentless competition on the supply side. It also provides incredibly diverse and deep demand. Heymi Bahar of the IEA sees this as perhaps the technology’s biggest advantage. What is revolutionary about solar, he says, is that it “is addressed to all kinds of investors”. From the teacher in South Africa who buys a $2 charger for her phone to the company developing 10GW power plants, everyone who uses solar is buying basically the same product. “There is no other energy-generation tech where you install 1m or one of the same thing depending on your application,” says Rob Carlson, a technology investor; as he puts it in a white paper, “The Sun has won”.

The key to the way this demand grows is to be found in the industry’s “experience curve”. The degree to which processes get cheaper as production gets larger is frequently expressed in terms of the extent to which unit costs come down every time cumulative production doubles. From the mid-1970s to the early 2020s cumulative shipments of photovoltaics in

creased by a factor of a million, which is 20 doublings. At the same time prices dropped by a factor of 500. That is a 27% decrease in costs for each doubling of installed capacity, which means a halving of costs every time installed capacity increases by 360%. If you treat the late 2000s, when subsidies led to the creation of foundries producing polysilicon specifically for solar cells, as an inflection point, the rate is now over 40%.

THE GREEN members of the German coalition which kicked off the huge demand-establishing subsidies of the early 2000s liked the decentralisation they offered; the Social Democrats liked the prospect of developing a new manufacturing industry devoted to their production. Both sides also saw solar panels as weapons in the fight to decarbonise the economy—but not necessarily as particularly powerful ones. They offered a sort of greenness that only really worked if people radically reduced their consumption.

It took those leading the decarbonisation charge some time to appreciate that solar could in principle be much more than this. When Adair Turner, a grandee technocrat, became the first chair of Britain’s Climate Change Committee, an organisation mandated by parliament to lay out the path to net-zero emissions, solar was not a large part of its thinking. “We totally failed to see that solar would come down so much,” he says. “In 2008 we were thinking that capital costs would come down 19% by 2020. When we got to 2020 they were down 95%.” In the 2014 report which set the agenda for the Paris agreement of 2015, the Intergovernmental Panel on Climate Change placed far more emphasis on carbon-capture at fossil-fuel plants and on burning biomass than it did on photovoltaics.

Since then, though, solar has proved the stand-out of the pack. In 2015 BloombergNEF estimated that the levelised cost of electricity ( LCOE) for solar, on a global basis, was $122 per MWh, almost half as high again as the LCOE for onshore wind, then $83. The LCOE for coal in places without carbon prices at the time was $50-$75. Today both solar and onshore wind are in the low $40s, while coal remains much where it was.

Not only have solar panels been getting cheaper more quickly than wind power, they have done so while staying comparatively unobtrusive. For wind, more efficiency means putting bigger turbines higher into the sky on more massive pylons. Their two-dimensionality allows solar panels to be a lot less visible from a distance (and also very easy to ship; you can get 300 into a standard TEU freight container). Though covering tracts of arable countryside with them upsets some people in some places, by and large solar panels are popular: research finds they enjoy more “social licence” than any other form of energy generation, be it renewable, fossil-fuel or nuclear.

Cheap, plentiful, acceptable energy which is emissions-free at the point of generation; it might seem that the climate crisis is solved. There is a catch, though—in fact, two. Consumers want to be able to draw power at night. And the grids to which they look for it work on the basis of a “merit order”: everyone supplying the grid at a given time is paid the price needed to attract the marginal supplier of power.

This becomes terribly inconvenient when very lowcost power from solar (or wind) becomes a large factor in electricity supply. When there is a lot of solar power on a grid the price of electricity in the middle of the day can fall to zero, or below. Solar-rich grids in Spain, Portugal, Germany, France, California and Texas have all experienced negative wholesale power prices in recent months. Eventually all markets which install plentiful solar can expect something similar, which makes the potential profits of further solar investment in such markets seem limited.

But there are ways around those limits. They include long-distance connections; storage (especially batteries); increasing overall demand; and the innovation low prices always encourage.

Long-distance connections allow sunnier places to serve those more dimly lit. England could be powered by panels in Morocco, New England evenings served by Nevada afternoons. Making such connections takes time and money. But if the power that is plentiful and cheap at one end can command an attractive enough price at the other they make sense.

Batteries and other storage technologies allow ar

bitrage across time rather than space; energy generated at midday, when grid prices are low, can be sold back when the Sun sets and prices are higher. What is more, batteries, like solar cells, are mass producible and targets of Chinese industrial policy. As a result they are moving down an experience curve even steeper than solar’s. The Rocky Mountain Institute, a thinktank, calculates that the cost of a kilowatt-hour of battery storage has fallen by 99% over the past 30 years.

By providing an investment case for new solar in markets that are already seeing zero prices, batteries increase demand for panels. Take California. It first saw sunshine-driven negative prices on the grid in 2017, when it had about 19GW of solar installed. It has more than doubled its solar capacity since then in part because it now has 10GW of battery storage; there have been evenings recently when batteries have been the largest source of power on its grid. Things are moving even faster in Texas, where battery operators had revenues of $532m in 2023.

It is possible that batteries might move electricity in space as well as time. Lawrence Berkeley National Laboratory estimates that there are 2.6TW of generation and storage capacity queuing up for grid connections in America—enough to double the country’s installed generating capacity. This queue contains a full terawatt of solar power. SunTrain, in which Dr Carlson’s firm, Planetary Technologies, is an investor, sees this as a market for batteries with wheels

The company plans to use solar farms in places that have little to recommend them other than a railway line nearby as filling stations at which to charge heavy but cheap batteries built into goods wagons. A 100-car train similar to the ones that currently carry coal east from Wisconsin could deliver 3 gigawatthours to users. Dr Carlson describes a utility-boss’s jaw hitting the floor when he proposed that, instead of a multi-decade planning battle to build a high-voltage transmission line, SunTrain could meet the utility’s power-import needs with a couple of trains a day.

FOR THOSE who are unconvinced by such an apparently outlandish way of profiting from cheap power there is a much more tried and tested avenue. It is one of the ironies of solar power that much of its growth has been driven by relatively unsunny countries, notably those of northern Europe, where there has been little demand for additional energy. The global south has a lot of empty land, better access to sunshine and much more unmet demand.

Adani Green Energy, one of the world’s largest solar developers, has obtained the rights to build solar farms on two vast tracts of land in India, one in Gujarat, near the border with Pakistan, the other in Rajasthan. Each of them is large enough to take some 30GW of solar panels, says Sagar Adani, the company’s boss and the nephew of the larger Adani Group’s founder, Gautam Adani. At that size they would offer a capacity more than two-thirds as large as that which Germany has installed over the past 25 years; and because India has much more sunshine, they will produce more energy in a given year than all those German cells put together. Mr Adani says the firm is installing about 5GW of solar on this land every year.

India’s solar expansion, Mr Adani says, is driven by two factors: energy security and national finances. “India imports gas for fuel, transport, fertilisers. It imports oil, too.” These are the main reasons for the current-account deficit. “So when Ukraine is invaded, Indian energy goes for a toss…You can’t have 1.4bn people rely on geopolitical factors for their energy.”

Not that Mr Adani is against using geopolitics to his advantage when the opportunity arises. His firm is both an operator of panels and a manufacturer of them. Adani Green Energy buys almost all the kit it is installing in India from China or firms in East Asia connected to the Chinese supply chain. It exports some 90% of the panels it makes in-house to America, which has concerns about Chinese PV supply, at prices 10-15% higher than those it pays for its imports. As Mr Adani’s production scales up, and his costs fall, he will find himself in the strong position of being able to install homemade panels when it suits him, and Chinese-origin PV when it does not.

Mr Adani’s first-order reasons for India’s going solar do not include decarbonisation. India wants more energy from many sources; it is building coal plants and wind farms (the Adani Group is involved in both) as well as solar farms. Climate diehards argue that it would be better advised to build only solar and wind. By some calculations the capital expenditure needed to generate solar energy is now less than the fuel bill for a fully depreciated coal plant. But those calculations do not always account for the higher costs of capital in a country where such projects are not yet easily bankable, especially if you are not an Adani. Nor do they include the political issues raised by shutting down a coal industry which employs millions.

As in India, so in many other middle-income countries. In the absence of strong policies aimed at curbing carbon-dioxide emissions, solar power may add to overall capacity as much or more than it displaces existing plants. And in the absence of strong policy the existing or potential capacity which it displaces will often be that which is clean, or cleaner, and comparatively expensive, not cheap and dirty coal. It is quite plausible to imagine there will soon be countries powered by solar, coal and little else.

It is also possible to imagine poor countries that quickly become mostly solar: in particular, countries in sub-Saharan Africa. Small-scale solar is already common across the continent. One barrier to a broader roll-out is financing. “These projects require financing upfront,” says Jehangir Vevaina of Brookfield, one of the world’s largest solar developers. “Investors need to have confidence that contracts will be honoured.” Lack of that confidence, stemming from the likelihood of political instability, means that investors demand high interest rates to finance African solar projects, increasing costs beyond the point of viability even when panels are cheaper than ever. Another problem is the parlous state of the continent’s electricity grids.

This means that, for the time being, solar power’s growth in sub-Saharan Africa will be more off-grid than in other regions (see Middle East and Africa section). Off-grid, its competition is mostly diesel power, which is much more expensive. Solar with batteries should be able to replace a lot of diesel generators and reduce the market for new ones very quickly.

One factor will be the spread of electric vehicles: an important driver in much of the world, but perhaps a particularly crucial one in Africa. Electric vehicles can be cheaper than those powered by internal combustion. Their batteries provide storage as part of the purchase price. And if powered by local renewables they drastically reduce fossil-fuel imports. This is the

logic which has led Ethiopia to ban the import of vehicles which use internal combustion. Though in Ethiopia the renewable energy in question is mostly hydropower, and the grid which delivers it unreliable, across much of the continent the energy will be solar and may not be delivered over a grid at all.

Africa currently has the lowest electricity use per person of any continent; 600m people in sub-Saharan Africa enjoy no access to electricity at all. For the continent’s average electricity use per person to rise to the level of India’s, which is more than twice as high, would require 2TW of new solar. Ten years ago that would have been unthinkable. At today’s prices it is beginning to look plausible. In ten years time, it should be well on its way to being done, and ambitions will have increased. And so demand will grow, and cumulative capacity will grow, and prices will fall.

PROVIDING BILLIONS of people in developing countries with the benefits of access to energy represents a huge amount of demand. Unmet need for air conditioning alone is in the terawatts, and will only grow as the population and temperatures rise.

But cheaper-than-chips solar will also stimulate innovations that increase electricity demand further everywhere. William Jevons, a 19th-century economist, pointed out that when energy gets cheaper, people use more of it. When that energy has large uncosted externalities, as fossil fuels do, Jevons’s “rebound effect” can be a source of environmental worry even as it provides economic benefits. If the energy’s only large cost is that of the marginal land in a place with a grid connection—or, if the user is willing to move nearby, without even that—it becomes a lot more benign.

SunTrain is one example of this sort of thinking. Another is Terraform Industries, a startup founded by Casey Handmer in 2021 to make “green hydrogen”.

Green hydrogen is made by powering electrolysers which split water into hydrogen and oxygen with renewable energy. Mr Adani thinks that a good chunk of his company’s solar output in India will be used this way to ease India’s reliance on imported natural gas. Green hydrogen is also much touted as a way of storing energy for longer periods of time than batteries offer. But the cost of the electrolysers needed makes it expensive. Mr Adani says that “India today is already at a place where the cost of green hydrogen is equal to the 10-year average of imported LNG [liquefied natural gas]”, but not everyone agrees—and even if it is indeed the case, LNG is a pricey form of energy.

Dr Handmer, formerly of the Jet Propulsion Laboratory in Pasadena, thinks that this approach is based on economic assumptions which no longer apply. People have assumed that, because electricity has a cost, it is a good idea for electrolysers to turn as much of the electrical energy fed into them into hydrogen as possible. The technologies which improve this hydrogen yield—platinum-group-metal electrodes, high pressures and temperatures, fancy membranes, heat exchangers—make the electrolysers expensive. That means they have to be used as close to 24/7 as possible to pay back the capital invested in them.

What if, instead, you produce an electrolyser with no bells and whistles that uses 60% more electricity to produce a unit of hydrogen but requires much less capex. And then you site it right next to the simplest sort of solar system imaginable—one which provides power in the direct-current ( DC) form that photovoltaics produce and electrolysers use, and thus does not need the inverters most systems use to put electric power onto the grid in the form of alternating current ( AC). You may need much more electricity to produce a unit of hydrogen than fancy-electrolyser systems do. But with very cheap electricity and huge savings on capital expenditure you can still come out ahead.

Terraform says that a cheap-electrolyser/off-grid-solar demonstrator it has built along these lines produces hydrogen at a cost close to $1 per kg, the level which analysts reckon hydrogen must reach in order to compete with fossil fuels. That it is well-suited to developing markets is not a coincidence. Mr Handmer thinks people should be able to “throw solar panels on the ground and hook up some equipment, anywhere on Earth”, in order to make any hydrogen they need.

Once you start to think in terms of energy being really copious and all-but free, at least at some times and in some places, brute-force approaches to all sorts of problems begin to appear. One way to drastically reduce the spread of airborne disease is to speed up the rate at which the air in the world’s buildings is vented and refreshed. If energy is expensive this is not feasible. But what if…? One way to remove carbon dioxide from the atmosphere is to grind certain sorts of rock into fine dust that is then dispersed across the oceans. Given that this needs to be done at a scale of billions of tonnes a year, again the energy requirement is incredible. And again, what if…?

Energy is not the only expense; any given scheme along these lines could fail. But that human ingenuity finds useful things to do with better access to energy is one of the clearest messages of the past 200 years. If real energy costs drop dramatically across the global economy, and access to energy expands, to bet against great things is to bet against the innovative engines of capitalism. It is not a wager history encourages. ■